7 Questions to Ask a Cash Home Buyer Before Signing

Selling your home for cash is often the fastest way to liquidate real estate, but the lack of regulatory oversight in the private investor market requires sellers to be hyper-vigilant. In 2024, institutional and private cash buyers accounted for approximately 28% of all residential transactions. While many are legitimate, the rise of ‘wholesaling’ and predatory ‘we buy houses’ scams makes interviewing real estate investors a critical step in protecting your equity.

To vet a cash home buyer effectively, you must verify their liquidity, track record, and contract transparency. The most critical questions for cash buyers involve confirming proof of funds, identifying the actual end-buyer, and clarifying who covers closing costs to ensure the net offer matches your expectations.

Why Vetting Cash Offers is Essential

Unlike traditional buyers who use mortgage lenders (providing a layer of bank-driven due diligence), cash buyers operate independently. This means the burden of verification falls entirely on the seller. According to industry data, nearly 15% of private cash offers fail to close due to ‘re-trading’ (dropping the price during the inspection period) or lack of actual capital.

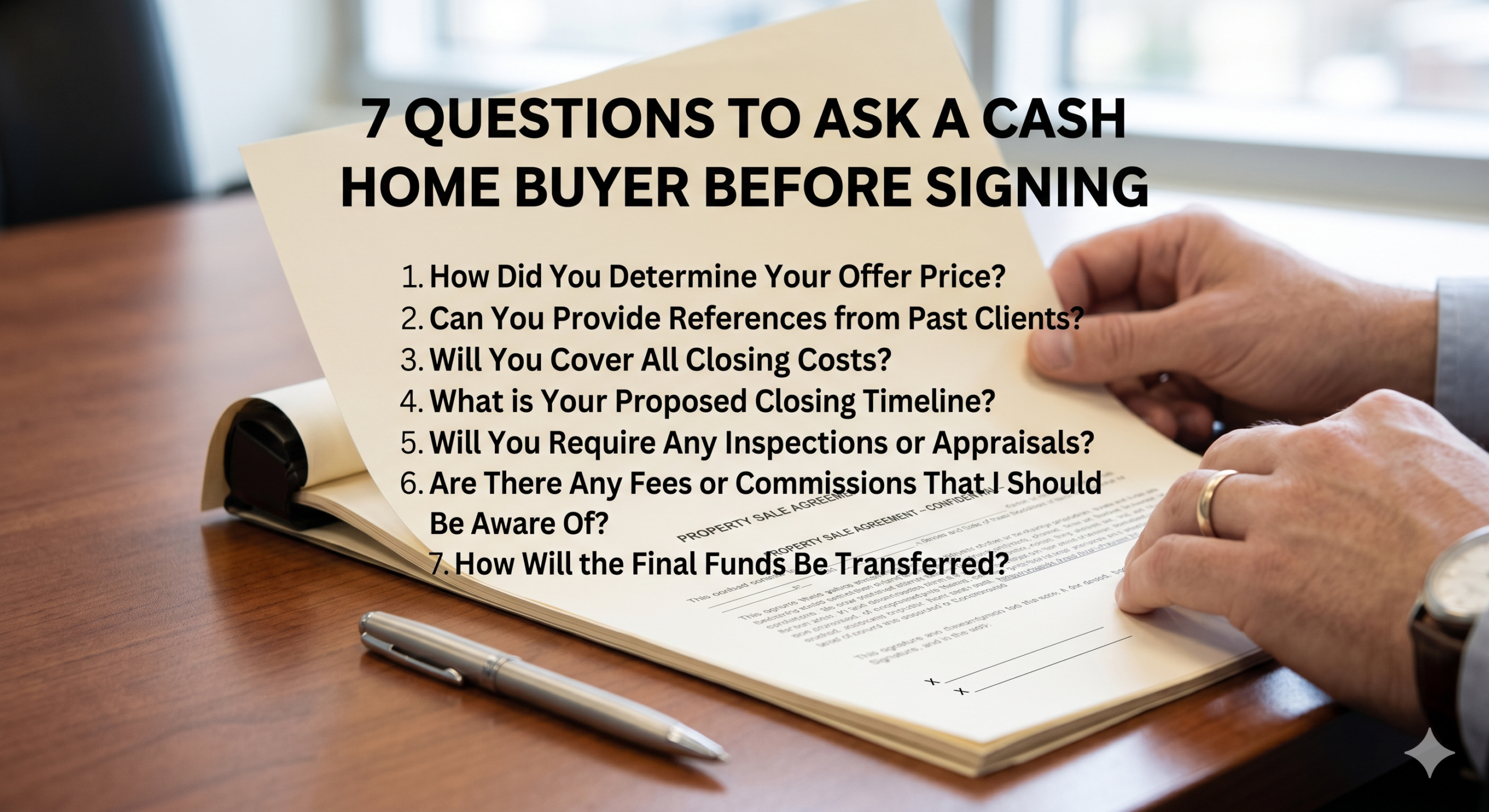

The 7 Essential Questions for Cash Buyers

1. Can You Provide a Recent Proof of Funds (POF) Letter?

A legitimate cash buyer should have the capital readily available. A Proof of Funds is a document (usually a bank statement or a letter from a financial institution) showing that the buyer has the liquid assets to cover the full purchase price.

- Red Flag: The buyer provides a ‘pre-approval’ letter or a ‘Letter of Intent’ from a hard money lender instead of actual bank statements.

- What to look for: The name on the bank statement should match the name of the LLC or individual on the purchase agreement.

2. Are You the End Buyer or an Assignee (Wholesaler)?

Many ‘cash buyers’ are actually wholesalers. They sign a contract with you and then ‘assign’ that contract to a third-party investor for a fee. While not illegal, this adds a layer of risk. If they can’t find an end buyer, they may back out of the deal at the last minute.

3. What is Your Proposed Timeline for Closing and Due Diligence?

The primary benefit of a cash sale is speed. A typical cash transaction should close within 7 to 21 days. If a buyer asks for a 45-day closing window or an extended 15-day inspection period, they may be trying to ‘shop’ your contract to other investors.

4. Who is Responsible for Closing Costs and Fees?

In most professional cash transactions, the buyer covers 100% of the closing costs, including title insurance, escrow fees, and transfer taxes. Vetting cash offers requires looking at the ‘net’ amount you receive, not just the gross offer price.

| Expense Item | Traditional Sale | Professional Cash Buyer |

|---|---|---|

| Agent Commission | 5% – 6% | 0% |

| Closing Costs | 1% – 3% (Split) | 0% (Paid by Buyer) |

| Repair Credits | Required after Inspection | Sold ‘As-Is’ |

| Timeline | 30 – 60 Days | 7 – 14 Days |

5. How Much Earnest Money Are You Putting Down?

The Earnest Money Deposit (EMD) is the buyer’s ‘skin in the game.’ For a cash offer, a deposit of 1% to 3% of the purchase price is standard. If a buyer offers a mere $100 or $500 deposit on a $300,000 home, they have very little to lose if they walk away.

6. Can You Provide References from Recently Closed Transactions?

Ask for the addresses of the last three properties they purchased in your area. A reputable investor will have a track record you can verify through public records. Check the county recorder’s office to see if the buyer’s LLC actually appears on the deeds of those properties.

7. Is the Offer Contingent on Any Outside Factors?

A true cash offer should be non-contingent. This means it is not dependent on them selling another property, securing a loan, or getting an appraisal. If the contract has a ‘financing contingency’ hidden in the fine print, it is not a true cash offer.

Performance Metrics: What a ‘Good’ Cash Offer Looks Like

When evaluating multiple bids, use these technical benchmarks to determine the strength of an offer:

- Offer Ratio: Typically 70% to 80% of After Repair Value (ARV) minus repair costs.

- Inspection Period: Should not exceed 5 business days.

- EMD Status: Should be held by a neutral third-party Title Company, not the buyer directly.

Frequently Asked Questions (FAQ)

What is the biggest risk when selling to a cash buyer?

The biggest risk is ‘Price Dropping’ or ‘Re-trading.’ This occurs when a buyer makes a high initial offer to get you under contract, then uses the inspection period to demand massive price reductions, knowing you are already committed to the move.

Do I still need a lawyer for a cash sale?

Yes. Even in a cash sale, having a real estate attorney review the ‘Agreement of Sale’ is highly recommended to ensure there are no predatory clauses or hidden contingencies that favor the buyer exclusively.

How do I verify a ‘Proof of Funds’?

Call the financial institution listed on the document. While they may not give out private details, they can often confirm if the account exists and if the balance is sufficient for the amount stated in the letter.

Conclusion

Vetting questions for cash buyers is the most effective way to separate professional real estate investors from amateur wholesalers. By insisting on a verified Proof of Funds, a significant Earnest Money Deposit, and a transparent closing timeline, you can enjoy the speed and convenience of a cash sale without sacrificing your financial security.