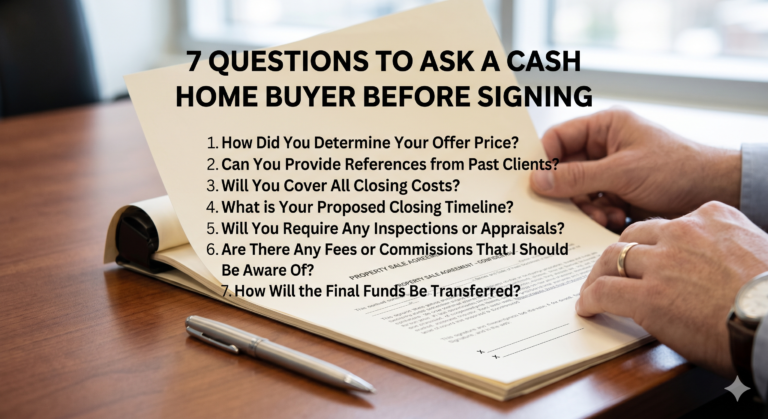

The Equity Protection Audit: Is Your Cash Offer a Lowball?

As the real estate market moves through 2026, all-cash transactions have stabilized, representing approximately 29% to 32% of all residential sales. While the allure of a fast, contingency-free closing is high, homeowners frequently struggle to differentiate between a legitimate investment offer and a predatory ‘lowball’ bid. To safeguard your financial future, conducting a lowball cash offer…