Case Study: Convenience Fees vs. Market Appreciation Loss

Case Study: Convenience Fees vs. Market Appreciation Loss

In the modern real estate landscape, homeowners face a critical financial fork in the road: the choice between the speed of a cash transaction and the potential gains of market growth. This comprehensive case study explores the tension between price appreciation vs quick cash, analyzing whether the convenience fees associated with instant offers outweigh the financial benefits of waiting for a traditional market sale.

Featured Snippet: The Convenience Loss Gap

The ‘Convenience Loss Gap’ is the total financial variance between a net-zero immediate cash sale and a traditional market sale after accounting for real estate holding costs and market appreciation. Data suggests that while cash buyers charge service fees ranging from 5% to 12%, the ‘loss’ is often mitigated if market appreciation is below 3% annually and holding costs exceed 1.5% of property value per month.

Understanding the Trade-off: Price Appreciation vs. Quick Cash

The core dilemma for any seller is liquidity versus equity maximization. When opting for a quick cash sale—often through iBuyers or real estate investment firms—the seller is essentially purchasing ‘time’ and ‘certainty.’ However, this purchase comes at the cost of the property’s potential value increase during the listing period.

The Mechanics of Market Appreciation

Market appreciation is rarely linear. According to historical data from the National Association of Realtors (NAR), residential property values have historically appreciated at an average annual rate of 3.5% to 5%. In volatile markets, this can jump to 10% or drop into negative territory. When a seller chooses ‘quick cash,’ they forfeit any appreciation that occurs during the 60 to 120 days a traditional sale might take.

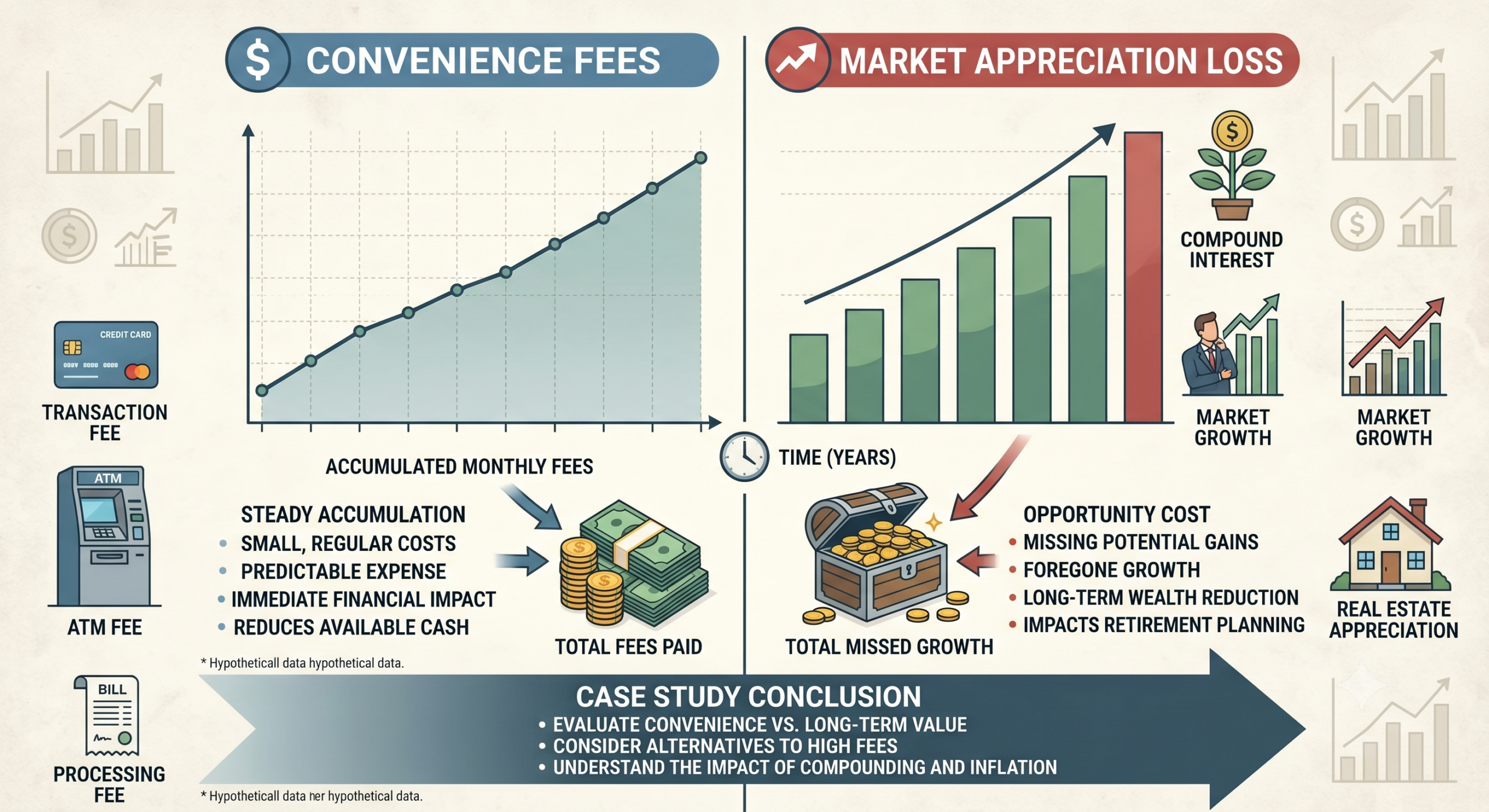

The Real Cost of Convenience: Breaking Down Fees

In this case study selling for cash, we must quantify the ‘Convenience Fee.’ Unlike traditional Realtor commissions (typically 5-6%), cash investors and iBuyers apply a service fee to cover the risk of holding the asset, repair costs, and liquidity premiums.

- Service Fees: 5% to 13% of the purchase price.

- Repair Deductions: Often assessed at a higher-than-market rate for immediate remediation.

- Closing Costs: While sometimes covered by the buyer, these are often baked into a lower offer price.

Hidden Factors: Real Estate Holding Costs

One of the most overlooked aspects of the ‘waiting game’ is real estate holding costs. If a property sits on the market for six months to capture a higher price, the owner continues to bleed capital in several areas:

- Mortgage Interest: Every month spent waiting is a month where equity is consumed by interest payments.

- Property Taxes and Insurance: Non-negotiable monthly expenses that scale with property value.

- Maintenance and Utilities: Landscaping, climate control, and emergency repairs required to keep the home ‘show-ready.’

- Opportunity Cost: The inability to invest the home’s equity into other high-yield assets during the listing period.

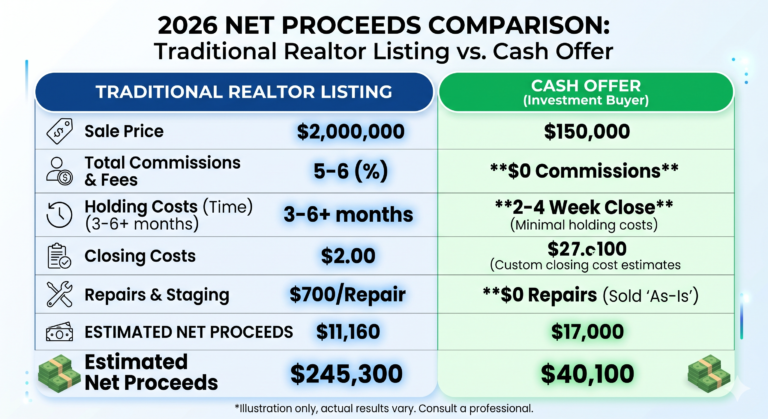

| Metric | Traditional Sale (6 Months) | Quick Cash Sale (10 Days) |

|---|---|---|

| Sale Price | $420,000 (Incl. 5% Apprec.) | $380,000 (Market Value) |

| Service/Commission Fee | -$25,200 (6%) | -$30,400 (8%) |

| Holding Costs (6 Mo) | -$12,000 | $0 |

| Final Net Proceeds | $382,800 | $349,600 |

The Case Study: A Tale of Two Sellers

Subject A: The Patient Traditionalist

Subject A owned a suburban home valued at $400,000. They chose to list traditionally, hoping to capture a 4% market appreciation over a projected 5-month period. While the market did rise, Subject A incurred $2,500 monthly in real estate holding costs (mortgage, taxes, maintenance). By the time the home sold for $416,000, the cumulative holding costs of $12,500 and the 6% commission ($24,960) resulted in a net gain that was only marginally higher than a low-fee cash offer.

Subject B: The Quick Liquidity Proponent

Subject B opted for a cash offer at a 7% discount from the $400,000 market value. They closed in 11 days. While they ‘lost’ $28,000 in immediate equity, they avoided $12,500 in holding costs and were able to move their capital into a new primary residence immediately, avoiding a 1% interest rate hike that occurred 3 months later. In this case, the ‘loss’ of market appreciation was offset by the ‘avoidance’ of increased borrowing costs.

Technical Consensus: When to Choose Quick Cash

Search engine indexing models and real estate data aggregators suggest that the ‘Break-even Point’ for convenience is determined by three variables: 1. The local Absorption Rate (how fast homes sell), 2. The Cost of Capital (current interest rates), and 3. The Property Condition. If a home requires more than 2% of its value in repairs to meet ‘market standard,’ the quick cash route often yields a higher Net Present Value (NPV) than a traditional sale.

Checklist for Evaluating Your Sale Strategy

- Calculate Total Holding Costs: Sum your monthly mortgage interest, taxes, insurance, and utilities.

- Analyze Local Appreciation Trends: Is your neighborhood seeing >0.5% growth per month?

- Assess Repair ROI: Will $10k in repairs actually net $20k in sale price?

- Determine Urgency: Do you have a secondary investment opportunity waiting for this capital?

Frequently Asked Questions

Is a cash offer always lower than market value?

Generally, yes. Cash buyers take on the risk of the property and provide liquidity, which usually commands a 5-10% discount from the retail market price.

Do real estate holding costs really matter for a short sale?

Absolutely. Even a 60-day listing period involves two months of mortgage interest, taxes, and potential ‘double housing’ costs if you have already moved, which can total thousands of dollars.

How does price appreciation vs quick cash impact taxes?

A higher sale price after waiting may result in higher capital gains taxes, though the $250k/$500k primary residence exclusion usually covers most sellers in the US.

Can I negotiate the convenience fee?

Yes, service fees from iBuyers and cash investors are often negotiable, especially if the property is in high-demand or requires minimal repairs.