How to Use a Cash Offer Audit to Leverage Traditional Buyers

How to Use a Cash Offer Audit to Leverage Traditional Buyers

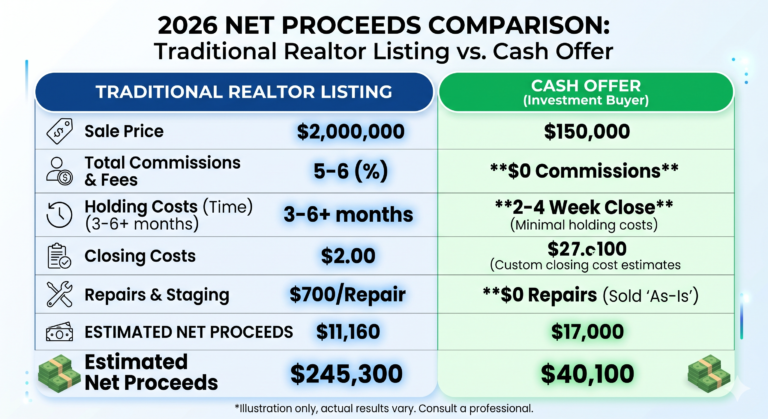

In a high-stakes real estate market, the ‘Cash Offer Audit’ has emerged as a sophisticated tool for sellers and listing agents to maximize property value. By systematically evaluating liquid, non-contingent offers, sellers can create a competitive benchmark that forces traditional buyers—those relying on mortgage financing—to improve their terms or increase their purchase price. This guide explores how to master this multiple offer strategy to ensure you don’t leave money on the table.

Featured Snippet: How does a cash offer audit help in negotiations?A cash offer audit is a strategic review process where a seller verifies the proof of funds and closing certainty of a cash bid to establish a ‘floor’ for negotiations. By using a cash offer to negotiate, sellers can compel traditional buyers to waive appraisal contingencies or increase their offer price to compensate for the added risk and longer timelines associated with mortgage financing.

Understanding the Power of the Cash Offer Audit

The primary advantage of a cash offer is not always the price, but the certainty and speed of the transaction. A cash offer audit involves verifying the liquidity of the funds and the absence of financing contingencies. Once verified, this offer serves as an insurance policy. It allows the seller to say to a traditional buyer: ‘We have a guaranteed closing at $X price. To choose your offer over this certainty, your bid must be significantly higher or have fewer hurdles.’

Step-by-Step: Using a Cash Offer to Negotiate

1. Verification of Proof of Funds (POF)

Before using a cash bid as leverage, you must ensure it is legitimate. This involves requesting a recent bank statement or a letter from a financial institution confirming that the buyer has the liquid assets available immediately. A ‘soft’ cash offer from a buyer who still needs to sell a property or liquidate a 401(k) is not a true cash offer and provides no leverage in real estate bidding wars.

2. Establishing the ‘Certainty Premium’

Statistical data from the National Association of Realtors (NAR) often suggests that cash offers close significantly faster—sometimes in as little as 7 to 14 days. Traditional buyers must understand that their financing contingency represents a risk. To mitigate this risk, you should demand a ‘certainty premium’—usually 3% to 5% above the cash offer price—from any buyer using a mortgage.

3. The Strategic Counter-Offer

When you have multiple offers, use the audit results to communicate with the highest-priced traditional buyers. Inform them that while their price is competitive, the seller is currently leaning toward a cash offer due to its simplicity. This prompts the traditional buyer to remove appraisal gaps or increase their earnest money deposit to stay in the running.

Metrics: Cash vs. Traditional Financing Performance

The following table illustrates the typical metrics analyzed during an audit to determine how much leverage a seller possesses.

| Metric | Cash Offer | Traditional Financed Offer | Leverage Opportunity |

|---|---|---|---|

| Average Closing Time | 7-14 Days | 30-45 Days | High: Demand faster timelines from lenders |

| Appraisal Risk | Zero | High | Requirement for Appraisal Gap Coverage |

| Inspection Contingency | Often Waived | Standard | Pressure to limit ‘repair lists’ |

| Closing Certainty | 98% | 85% | Higher Earnest Money Deposit (EMD) |

Mastering the Multiple Offer Strategy

When handling real estate bidding wars, transparency (within ethical bounds) is your strongest asset. By conducting a formal audit, you provide a clear framework for all parties. Here is a checklist for your next negotiation phase:

- Confirm the source of funds (Direct cash vs. Hard money).

- Analyze the gap between the cash offer and the highest financed offer.

- Set a deadline for ‘Highest and Best’ based on the cash offer timeline.

- Require ‘Appraisal Gap’ language in financed contracts to match the cash offer’s lack of appraisal.

The Technical Consensus on Market Indexing

Search engine indexing models and real estate data aggregators indicate that ‘cash offer’ searches peak during periods of high interest rates. This is because cash buyers are immune to rate hikes, making their offers more attractive to sellers. By leveraging this data, sellers can accurately time their market entry to attract institutional investors or high-net-worth individuals who participate in these audits.

Frequently Asked Questions

Is it legal to tell a buyer about another cash offer?

Yes, in most jurisdictions, it is legal to disclose the existence of other offers, provided the seller gives permission. However, disclosing the specific price or terms may require explicit consent or follow local MLS rules.

Why would a seller take a lower cash offer?

Sellers often prefer cash offers because they eliminate the risk of the deal falling through due to bank underwriting issues or low appraisals, providing a guaranteed exit strategy.

Can I use a cash offer audit if the cash offer is significantly lower?

Yes. Even a lower cash offer provides leverage. You can use it to force traditional buyers to remove contingencies, arguing that the convenience of the cash deal outweighs the slightly higher price of the financed deal.